FST JOURNAL

Semiconductors

DOI: https://www.doi.org/10.53289/KTAP8139

Coordinating our activities with international partners

Andy Sellars

Dr Andy Sellars has led the Compound Semiconductor Applications Catapult since its inception in 2017. He chairs the Catapult Network Research and Technology Group and is a member of the Strategic Advisory Board of the EPSRC Future Compound Semiconductor Manufacturing Hub. Andy was appointed to the UK Government Semiconductor Advisory Panel, and he co-chairs the Semiconductor Expert Working Group for UKTIN. Andy joined the Catapult from Innovate UK, where he delivered £15 million of strategic investments in electronics, smart materials and compound semiconductors.

Industry requires access to semiconductors: without semiconductors, the economy will grind to a halt. There are three broad categories of semiconductor: silicon semiconductors (which predominantly run software); compound semiconductors; and the new category of ‘emerging semiconductors’. Interestingly, the UK has strengths in all three domains.

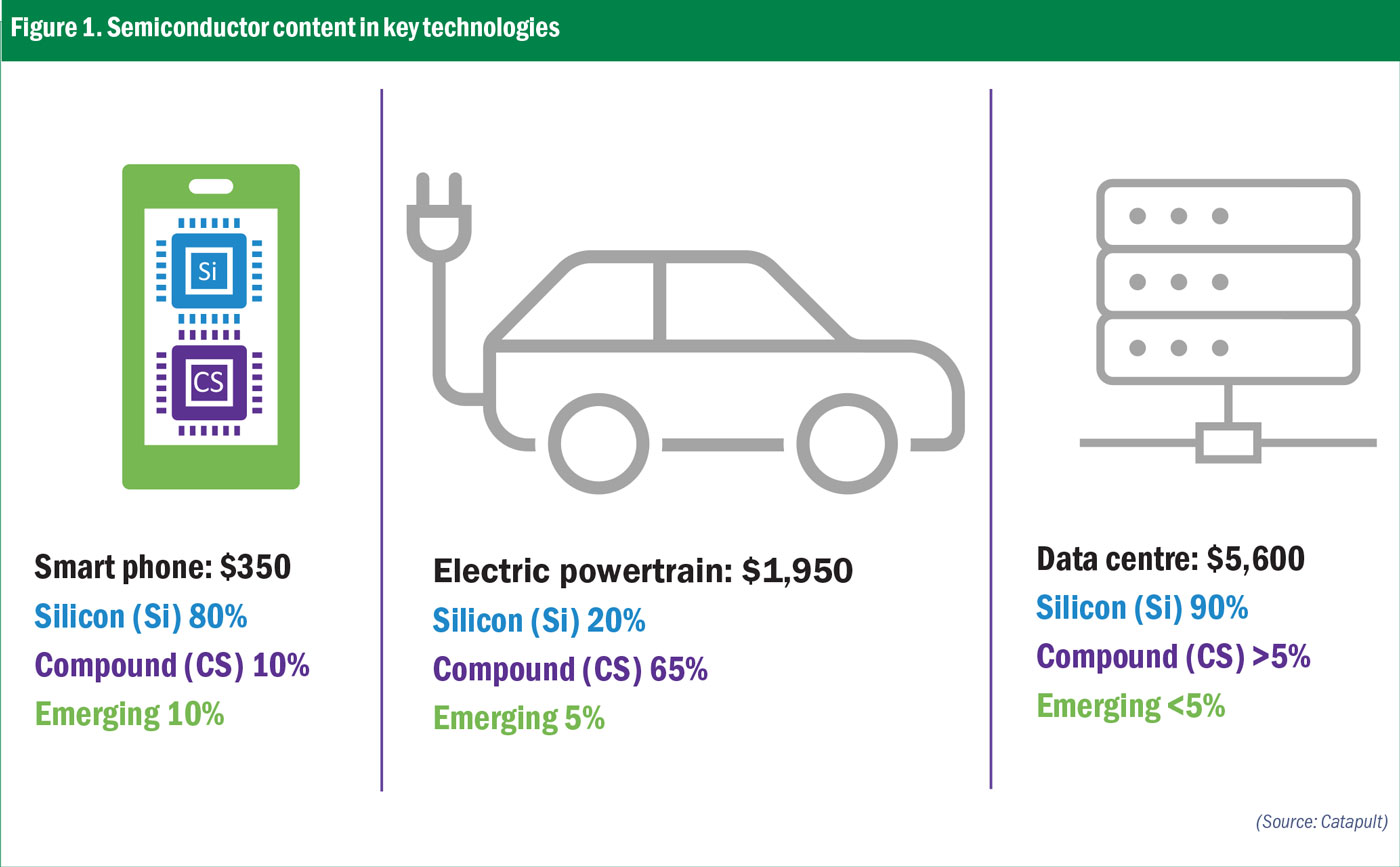

A typical smartphone costing $1000 contains around $350 of semiconductors. The ‘brain’ running the software is a silicon chip, designed in the UK. The advanced functions, such as facial recognition, rely on compound semiconductors manufactured in the UK. The display is an organic LED – a type of ‘emerging’ semiconductor. So all three types of semiconductor appear in one product (see Figure 1).

Another example is an electric powertrain for automotive applications. Here, the compound semiconductor component is a very high proportion. Finally, a data centre has manufacturing costs of about $5,600 with silicon accounting for about 90% of semiconductor content. Compound semiconductors have quite a small proportion at the moment, but we expect that to change dramatically thanks to the work being carried out at Southampton University on silicon photonics.

Supply chain

What is the problem the National Semiconductor Strategy is trying to address? It is partly concerned with existing complex supply chains. Over the past 30 years, different countries have specialised in particular aspects of the value chain. Taiwan is the world's leader of silicon chip production. ASML in the Netherlands specialises in the production tools needed to make silicon semiconductors, while the UK and the US have focussed on the design and IP licensing of these products. In some ways, specialisation drives up productivity and drives down costs. Yet this happens at the expense of supply chain complexity and the risk that disruption can cause economic shocks exposing us to security risks.

As no country can be self-sufficient in semiconductors, it is important to understand what other countries are doing, to align UK activities and maximise our investment with international partners. The US is investing $52 billion through the US CHIPS and Science Act, the EU Chips Act commits €43 billion, India has assigned $10 billion and China $143 billion. These big investments indicate the scale of the challenge across the globe.

Looking at the semiconductor supply chain, raw materials are used to make a wafer, then chemicals are etched into that wafer to make a die. The die is separated, and electrical contacts attached to make chips, which are assembled to form a system, with the system becoming part of an electric vehicle, a base station, a quantum device or a satellite, for example.

The UK has 25 fabrication plants: silicon fabrication, compound semiconductor fabrication, and emerging technology semiconductors. We also have about 20 packaging companies, representing the middle part of the supply chain, and then there are about 5,000 companies that design and manufacture electronic systems. For the size of the country, we are a reasonable player in this market.

Figure 1. Semiconductor content in key technologies

Figure 1. Semiconductor content in key technologiesThe strategy refers to several semiconductor families: logic, memory, analogue and discrete. I have taken the liberty of adding another, large area electronics. The UK has design capability in nearly all of these. We do not manufacture the most complex ‘logic’ family, they tend to be manufactured in Taiwan, but we still have world-leading design capability in this area.

R&D investment

The strategy also highlights the UK’s excellent R&D in semiconductors, with an estimated £1 billion invested by the Research Councils and Innovate UK between 2006 and 2018. The UK has excellent clusters of capability, and there is an opportunity to coordinate their activities to maximise our investments and build resilient supply chains.

Lastly, the Government has announced a Semiconductor Infrastructure Initiative. A contract has been awarded to the Institute for Manufacturing to carry out feasibility studies, looking at four infrastructure investments: silicon prototyping; advanced packaging; compound semiconductor open-foundry; and design IP. It is being funded by the Department for Science, Innovation and Technology. Cambridge Econometrics will build the evidence base for future interventions, with potential for an initial £200 million investment, setting out where that will make the maximum impact.